Most individuals carry Insurance for their cars, homes, or even lives. Most of us, though, never stop overanalyzing what Insurance is and how it functions.

Regularly many peoples search on google for term life insurance, whole life insurance, licindia, term insurance, life insurance policy and life insurance companies, etc., related all details they need to Types Of Life Insurance Policies.

Insurance is a contract between an insurance provider and a policyholder that provides financial protection or loss compensation. Insurance policies shield policyholders from experiencing both large and small financial losses, including liabilities for losses or harm to third parties and damages to the insured or their property.

How does Insurance work?

Everybody or any business can find an insurance firm prepared to insure it for a particular cost. A variety of insurance policies are accessible. Car, health, homeowner, and life insurance are the most prevalent personal insurance categories. Most Americans have at least one sort of Insurance, which is required by law for drivers.

Businesses require a certain kind of insurance coverage that addresses the risks that particular businesses experience. For instance, fast-food establishments are required to have policies that cover harm or damage caused by frying. Car dealers are not exposed to this kind of risk, although coverage is necessary for the event of test drive-related damage or injury. Kidnapping and ransom (K&R), medical malpractice, and professional liability insurance, often known as default errors and Insurance, are only a few of the specific needs for which insurance plans are available.

Many Americans have been encouraged by COVID to assess their life and financial situation and make plans in case they don’t exist. According to a Forbes advice study, 46% of American respondents stated that the COVID pandemic made them think about getting life insurance or more life insurance.

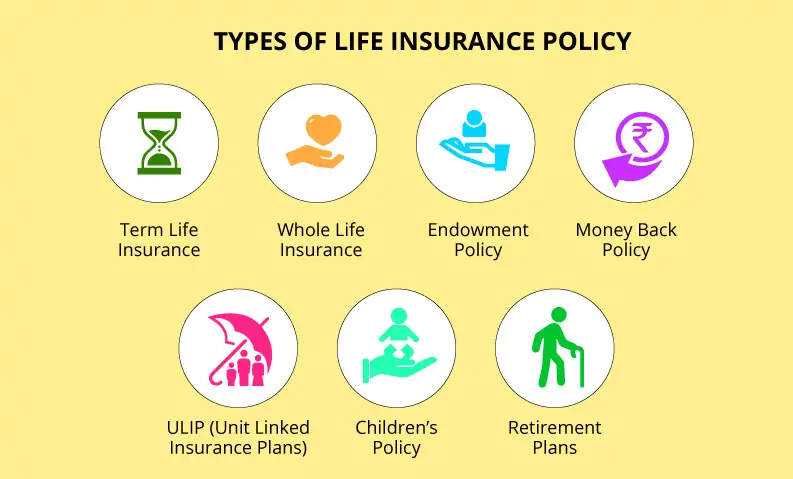

Term Life Insurance:

Basics: Futures life insurance has a set expiration date for as long as the premium stays the same. After this time, you can still amend the policy, but it will cost more each time. The options for coverage length are often 5, 10, 15, 25, or 30 years. It is the most affordable method of purchasing life insurance because you just pay for the insurance coverage and not the actual cost of the policy.

Who is virtuous: Futures life insurance is the best option for people who need life insurance protection for a certain debt or circumstance. For instance, some people purchase it as a means of income for their families, to cover their working years in the event that they pass away. To cover years of mortgages or other substantial loans, some people purchase term life insurance.

Cons: You might not see the improvement level as a touch if you still need coverage after the level is over. A new life insurance policy might also be highly expensive, depending on your age and any existing medical issues.

Whole Life Insurance:

Basics: Your life’s journey can be protected with whole life insurance. Using a portion of your premium payment, the account under the policy periodically generates cash value and accrues interest. A strategy would ensure that premiums wouldn’t go up, death benefits wouldn’t change, and cash prices would be withdrawn at a set rate.

Who It’s For: People who want life insurance and are prepared to pay a premium for the policy’s guarantee should consider their whole life.

Cons: Because of the assured characteristics, purchasing all life insurance is more expensive.

Universal Life Insurance:

The Basics: Due to its many variations and characteristics, universal life insurance might be complicated to comprehend. Because it typically does not provide the same guarantees as life insurance, a universal life (UL) can be less expensive. You can adjust the premium payment amount indications and compute the death benefit amounts across various constraints using particular universal life forms.

Suitable for: If a person wants lifetime coverage, universal life insurance may be a viable option. For people who want to compare their cash prices to market performance, some UL types are appropriate (Universal Variable Index and Life Insurance).

Disadvantages: Not all UL plans assure you will benefit if the monetary value is your primary concern. And let’s say you want to pay your premiums in a flexible manner. In that case, you should maintain a status above your policy status to prevent your cash value from being reduced or lost entirely due to costs and policy expenses. Recognize the UL policy’s guarantees and exclusions.

Variable Life Insurance:

Basics: Permanent protection is offered through conversion life insurance, which has no cash value. The sub-caps that should be invested and the rate of growth in the cash value are chosen by the policyholder. On the basis of your sub-khat performance, you can also lose money.

Ideal for: Those who desire active participation in their life insurance investments and lifelong coverage. Additionally, those who have convertible life insurance should not be afraid to take chances.

Cons: If you make the incorrect investment, you risk losing money on both your death and cash prices.

Mortgage Life Insurance:

The Basics: There is no mortgage life insurance because it is only intended to cover one mortgage sum. Two key aspects set this policy apart from the aforementioned kind of life insurance. First, hypothec lenders rather than your designated beneficiaries receive death payments. Second, if you have it insured, the payment is a mortgage or partial amount.

Who it’s for: Hypotech life insurance is designed for people who are particularly worried about having to pay off their mortgage after losing a loved one. It might also appeal to people who don’t want to undergo a medical checkup in order to get life insurance.

Downside:

Your family won’t have any financial freedom with this kind of policy. Future life insurance is preferable if you need life insurance to pay off a mortgage or other debts. You can give more than the money promised to your family and choose the term and amounts. The money can be used. However your family pleases. I hope you got all explain related to Life Insurance Policies.

People who have changed themselves beyond recognition (16 photos)

People who have changed themselves beyond recognition (16 photos)